The Fintech Opportunity on Cloud Marketplaces

Financial technology companies are entering a transformative era of distribution. Cloud marketplaces operated by AWS, Microsoft Azure, and Google Cloud have become major procurement channels for enterprises across every industry, and financial services is no exception.

According to industry analysts, cloud marketplace transaction volume exceeded $15 billion in 2025, with financial services software representing one of the fastest-growing categories. For fintech ISVs, this shift represents both a massive opportunity and a complex operational challenge.

The opportunity is compelling because the buyers are already there. Banks, insurance companies, asset managers, and payment processors are rapidly migrating to the cloud, and they increasingly prefer to procure their software through the same marketplace channels they use for infrastructure.

A 2025 Gartner survey found that 67% of enterprise financial institutions have established policies to prioritize cloud marketplace procurement for new software purchases. These buyers bring pre-approved budgets, streamlined procurement processes, and committed cloud spend that they are motivated to deploy.

However, fintech is unlike most other software categories when it comes to marketplace listing. The regulatory landscape surrounding financial services creates unique compliance requirements that ISVs must satisfy before their products can be listed, marketed, and sold through cloud marketplaces.

Understanding and addressing these requirements is the difference between a successful marketplace launch and months of delays, rejections, and missed revenue.

This playbook provides a comprehensive guide for fintech ISVs navigating the intersection of cloud marketplace distribution and financial services compliance. Whether you sell payment processing software, lending platforms, wealth management tools, or insurance technology, the frameworks and strategies outlined here will help you launch on cloud marketplaces with confidence and compliance.

The Regulatory Landscape for Fintech on Marketplaces

Fintech companies operate in one of the most heavily regulated sectors in the technology industry. When you add cloud marketplace distribution to the equation, you need to satisfy not only the regulatory requirements of your target market but also the compliance expectations of the marketplace operators and the institutional buyers who procure through them.

Understanding the key regulatory frameworks is the foundation for a successful marketplace listing strategy.

SOC 2 Type II

SOC 2 (System and Organization Controls 2) is the baseline compliance standard that virtually every enterprise buyer expects from cloud-delivered software. For fintech companies, SOC 2 Type II certification is non-negotiable.

Unlike Type I, which evaluates controls at a single point in time, Type II assesses the operating effectiveness of your controls over a sustained period, typically six to twelve months. Enterprise financial institutions will almost always require a current SOC 2 Type II report before they will approve a marketplace purchase, regardless of the marketplace's own vetting process.

The five trust service criteria covered by SOC 2, which include security, availability, processing integrity, confidentiality, and privacy, are all relevant for fintech applications. However, fintech companies should pay particular attention to processing integrity and confidentiality, as these criteria directly address the accuracy of financial data processing and the protection of sensitive financial information.

Your SOC 2 report should explicitly address how your application handles financial data, transaction processing, and regulatory record-keeping requirements.

PCI DSS

If your fintech product processes, stores, or transmits payment card data in any form, Payment Card Industry Data Security Standard (PCI DSS) compliance is mandatory. PCI DSS version 4.0, which became fully enforceable in March 2025, introduced significant new requirements around authentication, encryption, and continuous monitoring.

Fintech ISVs listing on cloud marketplaces must maintain their PCI DSS compliance independently of the cloud provider's infrastructure compliance. AWS, Azure, and GCP all maintain their own PCI DSS certifications for their infrastructure services, but your application layer compliance is your responsibility.

For marketplace listings specifically, you should clearly document your PCI DSS compliance level, your responsibility matrix showing the delineation between your controls and the cloud provider's controls, and any requirements that the buyer must satisfy in their own environment. This transparency accelerates the buyer's security review and reduces the back-and-forth that can delay marketplace deals by weeks or months.

SOX Compliance

The Sarbanes-Oxley Act (SOX) applies to publicly traded companies and their financial reporting processes. If your fintech software is used in financial reporting workflows, audit trails, or internal controls over financial reporting, your buyers will need to demonstrate that your software supports their SOX compliance obligations.

This does not require you to be SOX-certified yourself, but it does require you to provide SOX-relevant documentation including audit trail capabilities, access control configurations, data integrity controls, and change management processes.

GDPR and Data Privacy

Any fintech ISV serving European customers or processing data of EU residents must comply with the General Data Protection Regulation (GDPR). For marketplace listings, GDPR compliance affects how you handle customer data during the trial, purchase, and operational phases of the customer lifecycle.

Your marketplace listing should clearly disclose your data processing practices, identify the legal basis for processing, and provide mechanisms for data subject rights requests. Additionally, your Data Processing Agreement (DPA) should be readily available and compatible with the marketplace's transaction flow.

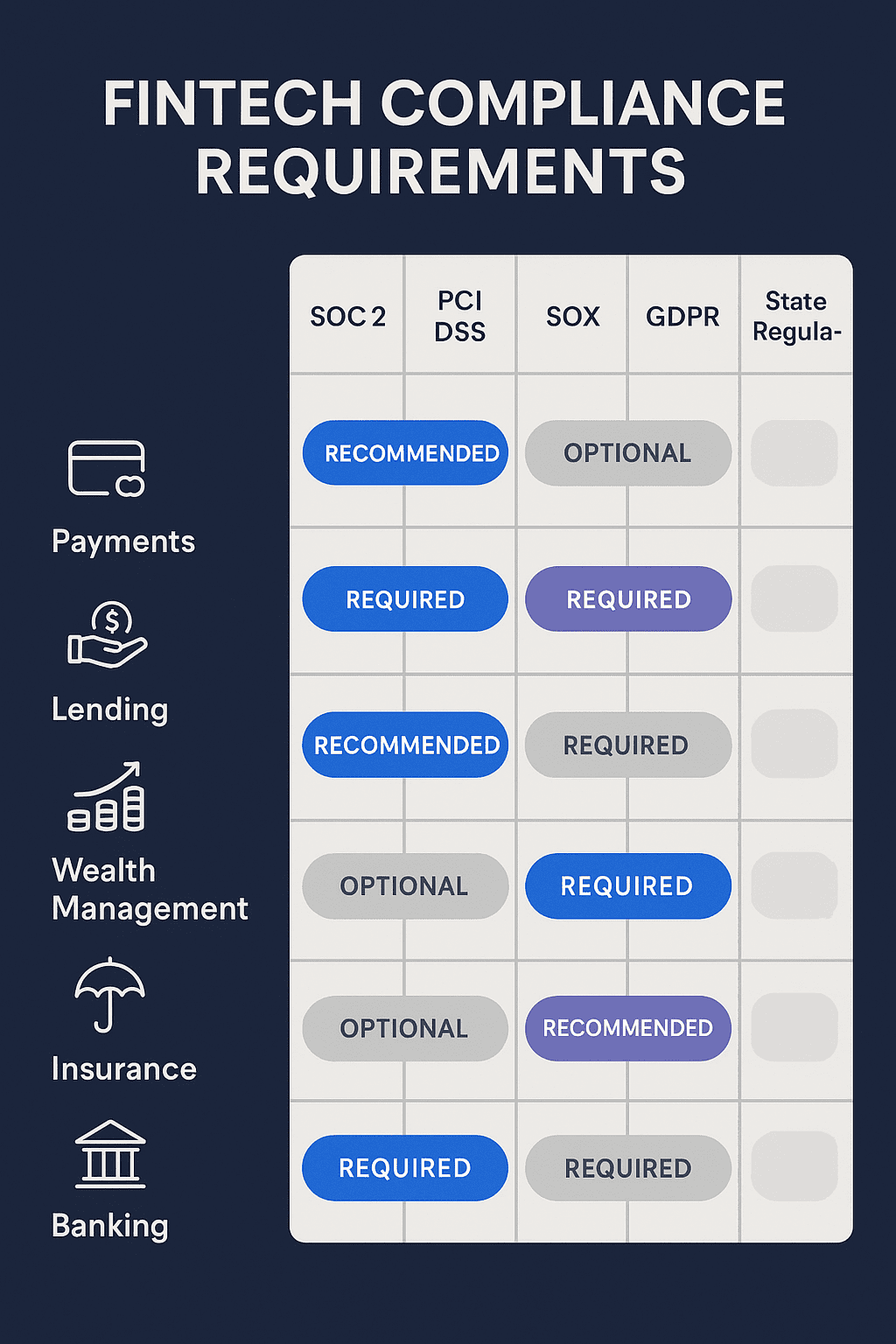

Compliance Requirements by Fintech Sub-Sector

The specific compliance requirements for your marketplace listing depend heavily on which segment of fintech your product serves. The following table provides a detailed comparison of the key compliance frameworks and requirements across major fintech sub-sectors to help you prioritize your compliance investments.

| Requirement | Payments | Lending | Wealth Management | Insurance |

|---|---|---|---|---|

| SOC 2 Type II | Required | Required | Required | Required |

| PCI DSS | Required (Level 1-4) | Situational | Situational | Situational |

| SOX Controls | Required for public buyers | Required for public buyers | Required | Required for public buyers |

| GDPR / Data Privacy | Required (EU operations) | Required (EU operations) | Required (EU operations) | Required (EU operations) |

| SEC / FINRA Regulations | Not typically | Situational (TILA, ECOA) | Required (Reg BI, Form CRS) | Not typically |

| State Licensing | MSB / MTL required | State lending licenses | State RIA registration | State insurance licenses |

| BSA / AML / KYC | Required | Required | Required | Situational |

| FFIEC Guidelines | Required for bank clients | Required for bank clients | Situational | Not typically |

| Data Encryption (at rest) | AES-256 minimum | AES-256 minimum | AES-256 minimum | AES-256 minimum |

| Data Encryption (in transit) | TLS 1.2+ minimum | TLS 1.2+ minimum | TLS 1.2+ minimum | TLS 1.2+ minimum |

| Penetration Testing | Annual minimum | Annual minimum | Annual minimum | Annual minimum |

| Business Continuity Plan | Required with RTO/RPO | Required with RTO/RPO | Required with RTO/RPO | Required with RTO/RPO |

This matrix should serve as a starting point for your compliance planning. The specific requirements for your product will depend on your exact functionality, your target buyer segments, and the jurisdictions in which you operate.

Engage legal counsel and compliance advisors with expertise in your specific fintech sub-sector to ensure comprehensive coverage.

How Regulated Financial Institutions Procure Through Marketplaces

Understanding the procurement process from the buyer's perspective is critical for fintech ISVs targeting marketplace distribution. Regulated financial institutions do not procure software the same way a technology company or a retail business does.

Their procurement processes are shaped by regulatory requirements, internal risk frameworks, and governance structures that add layers of review and approval beyond standard enterprise purchasing.

Vendor Risk Assessment

Before any financial institution can purchase your software through a marketplace, your company and product will undergo a vendor risk assessment. This assessment evaluates your financial stability, operational resilience, data security practices, regulatory compliance posture, and business continuity capabilities.

For marketplace purchases, the cloud provider's existing vetting provides some baseline assurance, but regulated buyers will conduct their own independent assessment regardless. Prepare a comprehensive vendor risk package that includes your SOC 2 report, penetration test results, insurance certificates, financial statements, and a completed SIG (Standardized Information Gathering) questionnaire.

Third-Party Risk Management

Financial regulators including the OCC, FDIC, and Federal Reserve require regulated institutions to maintain strong third-party risk management (TPRM) programs. Your software is classified as a third-party service, and the buying institution must demonstrate ongoing oversight of your service delivery.

Marketplace private offers can include custom terms that address these TPRM requirements, making them essential for enterprise fintech deals.

The Procurement Approval Chain

A typical marketplace procurement at a regulated financial institution involves business stakeholder sponsorship, IT architecture review, information security assessment, vendor risk management approval, compliance and legal review, and budget approval. The marketplace channel accelerates several of these steps, particularly budget approval when the buyer has committed cloud spend through programs like AWS EDP or Azure MACC.

However, the security and compliance review steps remain thorough regardless of the procurement channel. ISVs who prepare their compliance documentation proactively and make it easily accessible to buyer security teams consistently close deals faster.

Pricing Models for Fintech on Marketplaces

Fintech software uses diverse pricing models that do not always map cleanly to standard marketplace pricing structures. Choosing the right pricing model for your marketplace listing requires balancing your existing commercial model with the technical capabilities of each marketplace platform and the expectations of your financial services buyers.

Transaction-Based Pricing

Payment processors, fraud detection platforms, and transaction monitoring tools commonly use per-transaction pricing. AWS Marketplace and Azure Marketplace both support usage-based pricing through their metering APIs, making transaction-based pricing technically feasible.

The key challenge is implementing accurate metering that captures the correct transaction volume, reports it to the marketplace on the required cadence, and produces billing that matches the buyer's expectations. Fintech ISVs using transaction-based pricing should invest in strong metering infrastructure with reconciliation capabilities and transparent usage reporting for buyers.

AUM-Based Pricing

Wealth management and portfolio analytics platforms often price based on assets under management (AUM). This model can be implemented on cloud marketplaces through custom metering dimensions.

You define a metering dimension for AUM tiers and report the buyer's usage based on the AUM bands they fall into during each billing period. Private offers work particularly well for AUM-based pricing because they allow you to define custom pricing tiers that align with the buyer's specific portfolio size and growth expectations.

Per-Account or Per-User Pricing

Lending platforms, insurance administration systems, and banking software frequently use per-account or per-user pricing models. These models map naturally to marketplace subscription pricing with quantity-based tiers.

Consider offering both annual subscription pricing for predictable workloads and usage-based pricing for buyers whose account volumes fluctuate seasonally. This flexibility is especially important for fintech buyers who may experience significant volume variation during economic cycles or regulatory changes.

Platform License with Usage Overage

Many fintech products use a hybrid model combining a base platform license with usage-based overage charges. This model works well on cloud marketplaces through a combination of a fixed annual or monthly subscription for the base license and metered usage for overage consumption.

Structure your private offers to include the base commitment with clear overage rates, giving buyers cost predictability while maintaining upside revenue potential from growing usage.

Security Documentation and Certifications

Financial services buyers expect a level of security documentation that exceeds what most software categories require. Preparing this documentation before you list on cloud marketplaces eliminates a major bottleneck in the sales cycle and demonstrates the operational maturity that regulated buyers demand.

Essential Documentation Package

- SOC 2 Type II Report: Current report covering all five trust service criteria, with a bridge letter if your report is more than six months old.

- Penetration Test Results: Annual third-party penetration test report from a reputable firm, with evidence that identified findings have been remediated.

- Architecture Diagram: Detailed technical architecture showing data flows, encryption points, network boundaries, and integration touchpoints with cloud provider infrastructure.

- Data Flow Diagram: Specific documentation of how financial data enters, is processed within, and exits your system, including any third-party data sharing.

- Incident Response Plan: Documented procedures for security incident detection, containment, notification, and recovery, including SLAs for customer notification.

- Business Continuity and Disaster Recovery Plan: Documented recovery objectives (RTO and RPO), failover procedures, and evidence of regular DR testing.

- Encryption Standards Document: Detailed description of encryption algorithms, key management procedures, and certificate rotation processes for data at rest and in transit.

- Access Control Policy: Documentation of your access control framework including role-based access, multi-factor authentication, privileged access management, and periodic access reviews.

Marketplace-Specific Security Considerations

Each cloud marketplace has its own security review process. AWS Marketplace requires the Foundational Technical Review (FTR), Azure requires IP co-sell technical validation, and GCP has its own Partner Advantage technical review.

Fintech ISVs should budget additional time for these reviews, as financial services software typically receives more scrutiny than general-purpose business applications.

Co-Sell Strategies with Cloud Provider Financial Services Teams

All three major cloud providers maintain dedicated financial services industry teams that work closely with banking, insurance, and capital markets customers. These teams are valuable co-sell partners for fintech ISVs because they have deep relationships with the technology decision-makers at regulated institutions and understand the compliance requirements that govern procurement decisions.

Building Relationships with FSI Teams

Engaging the cloud provider's financial services industry (FSI) team requires a deliberate approach. Start by ensuring your marketplace listing is optimized with FSI-relevant keywords, compliance certifications, and use case descriptions that resonate with financial services buyers.

Register your co-sell opportunities through the appropriate partner portal, tagging them with financial services industry codes. Attend cloud provider-hosted FSI events and advisory boards to build direct relationships with the FSI specialists who influence procurement decisions at their banking and insurance customers.

Joint Solution Architectures

Cloud provider FSI teams are most engaged when you present a joint solution architecture combining your fintech software with the cloud provider's FSI-specific services. For example, pairing your fraud detection platform with AWS Financial Services Cloud or integrating your lending platform with Azure's banking-specific analytics creates a joint value proposition that makes it easier for the cloud provider's account team to champion your solution.

Compliance Co-Marketing

Use the cloud provider's own compliance certifications in your co-marketing efforts. Reference their certifications alongside your own to present a complete compliance picture addressing the buyer's end-to-end regulatory requirements.

Co-authored whitepapers, joint webinars, and shared case studies demonstrating compliant deployments on cloud infrastructure are powerful sales acceleration tools.

Case Study Examples

While specific company results are confidential, the following composite scenarios illustrate how fintech ISVs have successfully navigated marketplace listing and compliance challenges. These examples are based on patterns observed across multiple fintech marketplace launches and represent realistic outcomes for ISVs in each sub-sector.

Payments Platform: From 9-Month Sales Cycles to 6 Weeks

A payment processing ISV with PCI DSS Level 1 certification listed on AWS Marketplace with pre-built compliance documentation, a standardized private offer template, and transaction-based metering. By proactively sharing their SOC 2 report, PCI attestation, and pre-completed SIG questionnaire through a secure portal linked from their marketplace listing, they reduced the buyer's security review from an average of 12 weeks to 3 weeks.

Combined with the procurement acceleration from buyers using AWS EDP committed spend, their average enterprise deal cycle dropped from nine months through direct sales to approximately six weeks through marketplace. Within eighteen months, marketplace channel revenue grew to represent 40% of their total new business.

Lending Platform: Unlocking Bank Buyers Through Marketplace

A digital lending platform targeting community and regional banks listed on Azure Marketplace with Azure IP co-sell status and full FSI compliance documentation. By using Microsoft's existing banking relationships and compliance framework, they bypassed several layers of vendor assessment.

Their marketplace launch resulted in 23 new bank customers within the first year, compared to an average of 8 per year through direct sales.

Building Your Fintech Marketplace Compliance Roadmap

Launching a fintech product on cloud marketplaces is not an overnight initiative. A realistic timeline from compliance preparation to active marketplace selling spans three to nine months, depending on your current compliance posture and the complexity of your product.

The following roadmap provides a phased approach that balances speed to market with compliance rigor.

- Month 1-2: Compliance Audit and Gap Analysis. Assess your current compliance certifications against marketplace requirements and buyer expectations. Identify gaps in your SOC 2 coverage, penetration testing cadence, and security documentation. Engage your compliance team or external advisors to create a remediation plan.

- Month 2-3: Documentation Preparation. Prepare your security documentation package, including architecture diagrams, data flow documentation, compliance attestations, and a pre-completed vendor risk questionnaire. Create a secure portal or document room where buyer security teams can access this material efficiently.

- Month 3-4: Marketplace Listing Development. Build your marketplace listing with FSI-relevant positioning, compliance certifications prominently displayed, and pricing models configured for financial services buyer expectations. Implement metering infrastructure if using usage-based pricing.

- Month 4-5: Marketplace Technical Review. Submit your listing for the marketplace's technical review process. Address any findings promptly and use the feedback to strengthen your compliance posture.

- Month 5-6: Co-Sell Enablement. Register for co-sell programs, engage cloud provider FSI teams, and build your private offer playbook with compliance-focused templates designed for regulated buyers.

- Month 6+: Launch and Iteration. Go live on the marketplace, activate co-sell motions, and continuously iterate on your compliance documentation based on buyer feedback and evolving regulatory requirements.

How Automatum Accelerates Fintech Marketplace Success

Fintech ISVs face unique operational challenges when selling through cloud marketplaces. The combination of complex pricing models, stringent compliance requirements, and multi-stakeholder procurement processes demands tooling that goes beyond basic marketplace listing management.

Automatum provides fintech ISVs with the operational infrastructure they need to succeed on cloud marketplaces without building custom tools for every workflow.

With Automatum, you can manage private offers with custom compliance terms across AWS, Azure, and GCP from a single platform. Our metering integration supports the transaction-based, AUM-based, and hybrid pricing models that fintech products require.

Our analytics dashboard consolidates marketplace revenue, deal velocity, and customer engagement metrics so you can measure and optimize your marketplace performance. And our co-sell workflow automation ensures your opportunities are properly registered and tracked across cloud provider partner portals.

If you are a fintech ISV ready to expand your distribution through cloud marketplaces while maintaining the compliance rigor your buyers demand, visit automatum.io to learn how our platform can help you work throughity of regulated marketplace selling and accelerate your path to revenue.

Automatum simplifies cloud marketplace operations across AWS, Azure, and GCP.

Book a Working Session →Frequently Asked Questions

Common questions about the topics covered in this guide.

What compliance certifications do fintech ISVs need for marketplace?

At minimum SOC 2 Type II and PCI DSS if handling payment card data. SOX compliance is needed for financial reporting products. GDPR compliance is required for European operations. Many buyers also expect ISO 27001.

How do fintech companies handle data residency on marketplace?

Use cloud-native data residency controls: AWS Control Tower, Azure Policy, or GCP Assured Workloads. Financial services customers often require data to remain within specific geographic regions for regulatory compliance.

What is the AWS Financial Services Competency?

A partner designation that demonstrates validated financial services expertise. It provides a trust badge on your marketplace listing, access to financial services-focused co-sell opportunities, and priority placement for FSI buyers.

How should fintech ISVs price on marketplace?

Financial services buyers prefer predictable pricing with annual contracts. Use subscription-based pricing for platform access and add usage-based dimensions for transaction processing volume. Include premium SLA tiers for regulated workloads.

Keep building your marketplace motion

Compliance and listing guides for financial services ISVs.